As one rural town appeals to those sick of city prices to come and live there, John Cradden looks at the pros — and cons — of opting for country life

Amid soaring property prices and rents that are once again skewing the cost of living in urban centres, there's always the option of moving to the country where things seem considerably cheaper.

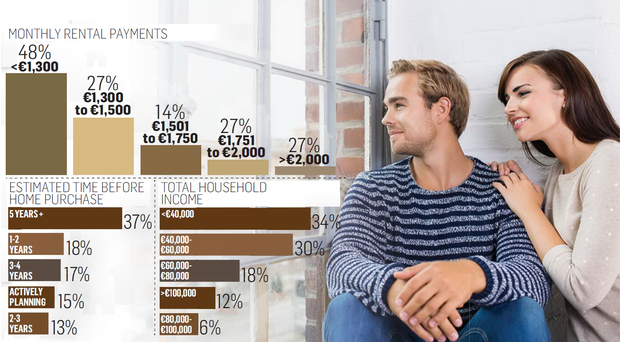

So instead of despairing at not being able to find a three-bed home in Dublin city for less than €400,000, or one to rent for less than €1,500 a month, you could move to an area where such a property could be bought for less than €100,000 or rented for less than a €100 a week.

In other words, perhaps a place like Kiltyclogher, Co Leitrim, a picturesque rural village with a population of 233 that recently started a campaign to attract new residents. The central purpose behind the KiltyLive campaign is to help prevent the loss of one of the two teachers at the local school, which has just 14 pupils registered for the coming year.

But while it's too early to say how successful the campaign will be, it could well spark off some serious thinking among those who, for whatever reason, are finding the financial pressures of city life just a bit much.

However, it can be difficult to find reliable data comparing the cost of living in urban vs rural areas. The CSO used to release figures comparing the cost of grocery shopping in Dublin vs outside Dublin, but this was stopped in 2009.

Property

At least as far as property prices and rents are concerned, there's no argument. According to figures from the monthly rental report of property website Daft.ie, the average mortgage repayment on a three-bed property in Co Leitrim during the first three months of this year was €310 a month compared with €2,015 for South Co Dublin.

In Co Kerry, a mortgage on a three-bed is averaging €446 while they can expect an average rental yield of €638. In Waterford city and county, three-bed homeowners pay an average of €515, while they could rent it out for between €680 and €764 a month.

It's only when you survey Ireland's fifth-largest city - Galway - that average rents start to hit the €1,000 mark, while the monthly mortgage on a three-bed will be around €830. Even the rebel city can't compete with the average rental yields or property prices in any part of Dublin city and county.

However, transport costs may well eat into some of the savings made by buying or renting outside the Pale. Decent public transport will be lacking in many regional towns, meaning a greater reliance on cars to get around. Many rural dwellers with school-going kids may not be able to benefit from the State's School Bus scheme because they are not close to any of the pick-up points.

On the plus side, you can still find some of the cheapest petrol stations in places like Dundalk, Waterford and Tralee, according to Pumps.ie, which lists the cheapest stations around the country. And car insurance is likely to be cheaper if you live in a rural area in Co Donegal or Cork, according to a survey by this newspaper a few years back.

But it's no surprise to find that childcare is cheaper outside Dublin, according to the CSO, which released figures last month showing that the average weekly cost of pre-school childcare in July to September last year was €150 in Dublin compared with €83 in the south-east and the mid-west regions. The national average cost per week is €118. Dublin also figured as the most expensive for non-parental childcare for pre-schoolers at €4.90 per hour compared with €3.50 for the mid-west and south-east.

In terms of utilities, rural dwellers can expect to pay as much as €54 a year more in electricity standing charges than their urban counterparts. Energia, for instance, charges rural customers with nightsaver meters €251.88 in standing charges, compared with €197.99 for urban-based dwellers.

But, of course, what constitutes value depends on who you ask, so all this data may only provide part of the picture for those looking for the cheapest places to live in Ireland. One website that has been collecting ratings and comments since 2009 about the cost of living in different parts of the country is Likeplace.ie.

Run by brothers Shane and Ronan Difily, it has a ranking of the cheapest to the most expensive places to live based on submissions from its users. Number one on the list is Letterkenny, Co Donegal, with a score of 3.4 out of five. "The higher the score the happier people are," said Shane. In other words, low costs equates to higher happiness and a high score, he adds.

Also in the top 10 for cost of living are Tuam, Dundalk, Youghal, Longford town, Carlingford, Bray, Schull, and Tralee. Not surprisingly, the place with the highest cost of living is Dublin city at 2.9 out of five, but there are quite a few urban places that rank quite highly.

"There is a good mix of rural-vs-urban in-between. In general though, you'll see that the spread is now very wide. All these scores come in at between 2.9 to 3.4-out-of-five," said Shane.

While these user ratings are entirely subjective (there are other ratings for things like law and order, sense of community, local services, and schools), the widening chasm in the cost of housing between and Dublin and almost everywhere else remains undoubtedly the biggest single factor that is prompting many a worker to up sticks to the country.

Unaffordable

Tralee man Shaun O'Shea used to live and work in Dublin before returning to live in his home town a few years ago, where he now heads up the local office of Sigmar Recruitment. Part of his motivation for moving home was the extent to which house prices and rents in Dublin were becoming unaffordable.

"A friend of mine bought a one-bed apartment in Dublin for €400k, but that would buy you sea views, and five bedrooms on an acre of land in Tralee."

While smaller towns like Tralee won't attract the numbers of regional urban centres like Waterford and Galway, it is definitely seeing an influx. "Up until 12 months ago, you wouldn't have been working in areas like Tralee or Waterford unless you're from that area. They don't have a natural pull but in the last year that has changed."

He says at least part of this is down to the growth in numbers of workers - many of them IT contractors - who are choosing to telecommute or become remote workers. One indication of this is the recently opening of a new shared office space with both one-person offices and a series of hot desks called HQ Tralee.

Lots of people living in Dublin are looking to return to places where they grew up," said O'Shea.

"With salaries, definitely in areas like IT, engineering and sales and marketing, there's not that much of a drop."

According to Sigmar Recruitment's salary guide, a Java software developer with three-five years' experience can expect to earn between €40,000 and €60,000 in Dublin, compared with €35,000 to €50,000 in the rest of the country. There seems little difference per region in the grades for sought-after jobs like a building site engineer, while a sales manager might only expect to earn a €5-€10,000 premium in earnings if he or she is based in Dublin.

But while swapping Kilmainham for Kiltyclogher might be a step too far for most of us, it is hoped that the new National Planning Framework will be more successful than the National Spatial Strategy in encouraging more Dublin-based families to consider migrating to other cities and regional towns.